Early last month, President Joe Biden signed the American Rescue Plan Act (ARPA) into law. A sweeping $1.9 trillion aid package, the ARPA is the latest major piece of legislation to provide economic relief and stimulus, both tax and non-tax, during the Covid-19 pandemic.

While the ARPA will help mitigate the continuing effects of the pandemic, the sheer vastness of this sixth major coronavirus relief package has left many feeling overwhelmed. To help you better understand the tax provisions in the ARPA, we have compiled brief summaries of the key aspects of the provisions affecting individuals and the provisions affecting businesses. For information on the provisions affecting individuals, read on! For information on the provisions affecting businesses, stay tuned! More information is coming next week.

As always, the Maddox Thomson & Associates team is here to help with any tax-related questions and concerns you may have. We are available at your convenience to discuss in more detail any of the ARPA changes and how they may apply to you.

Provisions Affecting Individuals

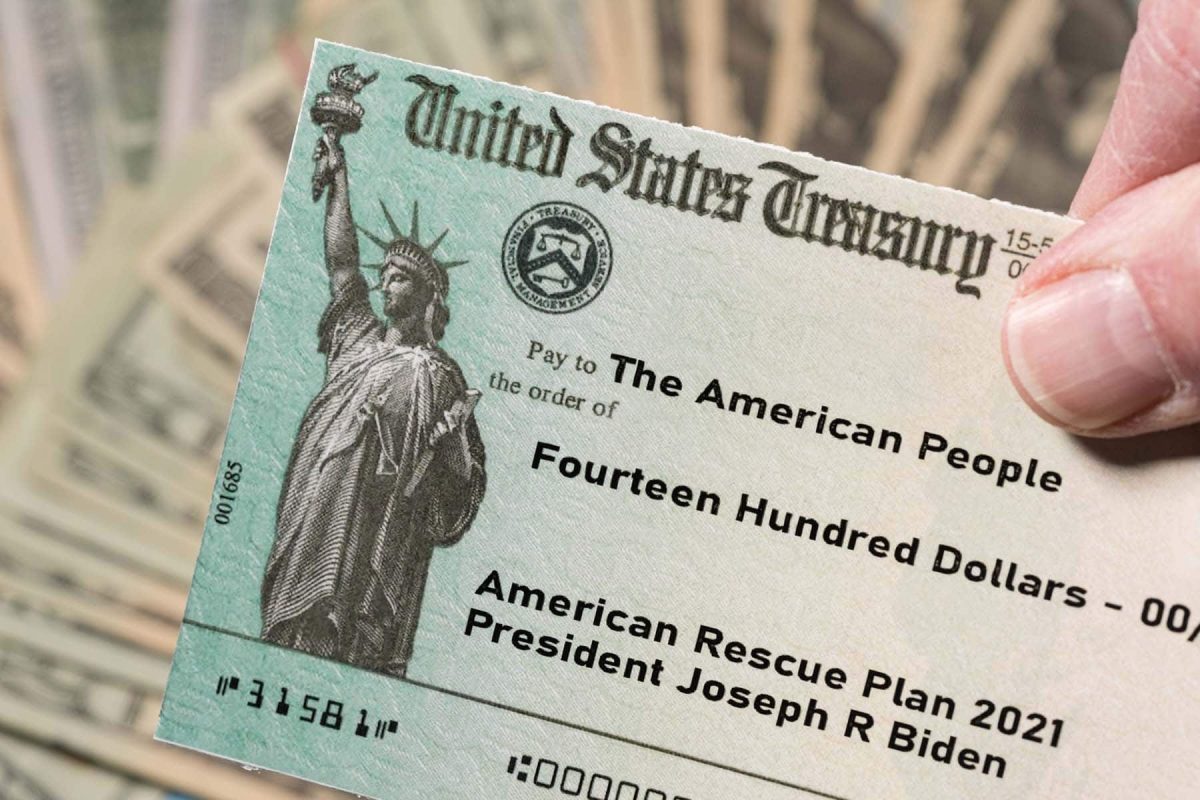

Recovery rebate credits (stimulus checks): ARPA provides a third round of nontaxable stimulus checks directly payable to individuals. The payments are structured as refundable tax credits against 2021 taxes but will paid in 2021 (not 2022).

The maximum payments are $1,400 per eligible individual ($2,800 for married joint filers) and $1,400 for each dependent (which, unlike the first two stimulus payments, includes older children and adult dependents). The payment phases out proportionally between $75,000 and $80,000 AGI for single filers, $112,500 and $120,000 for head of household filers, and $150,000 and $160,000 for married joint filers.

Rules for identification, for payments made notwithstanding no filing of 2019 and 2020 returns, and for limitations on offsets apply. Eligibility is based on information from 2020 income tax returns (or 2019 returns, if 2020 returns haven’t been filed when the advanced credit is initially issued). For households whose payment was based on 2019 income data, and who would be eligible to receive a larger payment based on 2020 data, IRS is directed to issue a supplementary payment.

Child tax credit (for 2021):

- Qualifying children include 17-year-olds,

- The credit is increased to $3,000 per child ($3,600 for children under six years of age), but the increase is subject to modified AGI phase out rules (and the existing modified AGI phase out rules for eligibility for any credit at all continue to apply),

- The credit is refundable, and

- IRS will make periodic advance payments totaling 50% of its estimate of the credit in the last half of 2021.

Earned income tax credit (EITC):

- For 2021 the credit is increased for taxpayers with no qualifying children and age restrictions for those taxpayers are relaxed;

- After 2020 taxpayers that have a qualifying child but can’t meet the identification requirements for the qualifying child are nevertheless allowed the credit;

- Taxpayers may use the greater of their 2019 or 2021 earned income in calculating the credit for 2021;

- After 2020, the amount of investment income that a taxpayer can have and still earn the credit is increased; and

- After 2020 there is broadening of the existing exception to the credit’s joint filing requirement under which separated married people eligible to file jointly are allowed the credit even if they don’t file jointly.

Child and dependent care credit (for 2021):

- The credit is refundable;

- The amount of qualifying expenses taken into account for the credit is increased from $3,000 to $8,000 if there’s one qualifying care recipient and from $6,000 to $16,000 if there are two or more;

- The maximum percentage of qualifying expenses for which credit is allowed is increased to 50% from 35%; and

- Phase-down rules, based on AGI, are changed.

The increased dependent care assistance program exclusion amount (see below) under Code Sec. 129 will also affect the child and dependent care credit, as the amount of expenses taken into account for the credit is reduced by the amount excludable from the taxpayer’s income under Code Sec. 129.

Dependent care assistance programs: For 2021, the amount excludible under a dependent care assistance program is increased to $10,500 (or $7,500 for a married taxpayer filing a separate return). Retroactive plan amendments are allowed to facilitate the increase.

Health care premium assistance credit: For 2021 and 2022, the credit will be available for a larger percentage of insurance premiums, and individuals whose income is greater than 400% of the poverty line will be eligible for (rather than barred from) the credit. For 2020, individuals who were provided advances of the credit under the Patient Protection and Affordable Care Act in excess of the credits to which they are entitled aren’t obligated to pay back the excess. And, notwithstanding any other rules, individuals who receive unemployment compensation during 2021 are eligible for the credit (and under rules that increase the amount of the credit).

Income exclusion for unemployment benefits: For 2020, taxpayers with modified AGI less than $150,000 can exclude from gross income $10,200 of their unemployment benefit. The exclusion is available to each spouse if a joint return is filed. For taxpayers who already filed 2020 returns and did not exclude unemployment benefits, IRS said that taxpayers shouldn’t file an amended return and that additional guidance will be provided.

Student loan forgiveness: Beginning in 2021 and continuing through 2025, the forgiveness of many types of loans for post-high school education won’t result in income inclusion for the forgiven amounts.